The Indian Banking Licenses Story

In today’s digital era, the Indian banking sector is considered one of the most evolved banking systems in the world. With healthy competition thriving between the public and the private sectors, the banking sector in India has a variety of players that work within the ambit of varying banking licenses and legal frameworks. To understand the Indian banking sector better, it helps to know about the various banking licenses that are in place today.

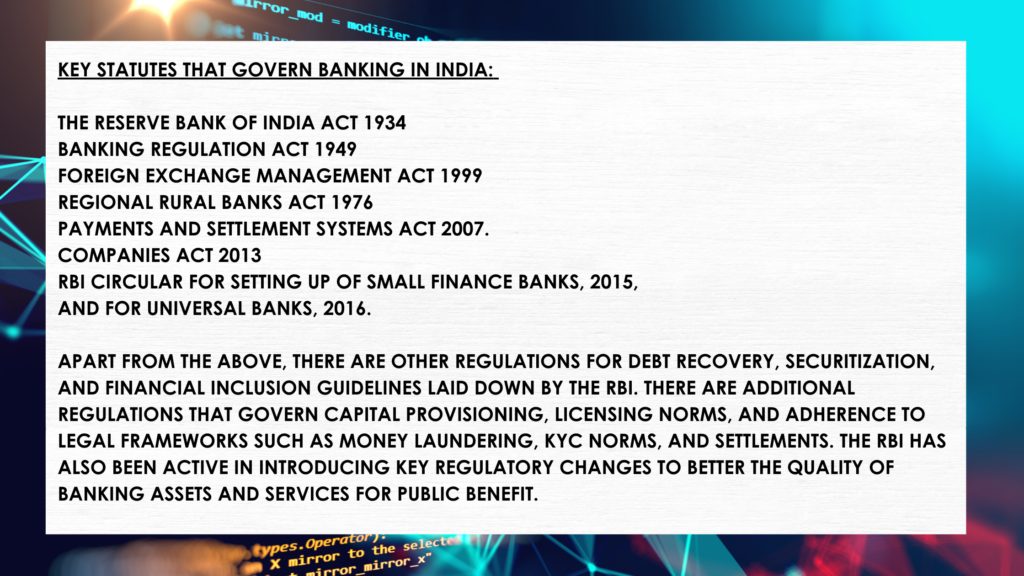

Established in 1935, the Reserve Bank of India (RBI) is the central bank of the Indian union, that is empowered to license banks, with the ability to dynamically adapt and formulate newer frameworks that govern how banking institutions are run in the country. During the first few decades after Indian independence, the country followed a cautious approach to banking licenses, with limited numbers given after strong scrutiny, with a fillip to public ownership.

Thus, until 1993, banking licenses were a hard-to-get privilege in India, often restricted to banking schedules and governmental approvals, and were finite in their limits. After the liberalization policy changes, India extended licenses to the private sector, pivoting policy from a nationalization approach followed in the 1960s and 70s to herald a new era of competitive, internationalized banking in India.

Information about banking licenses in India

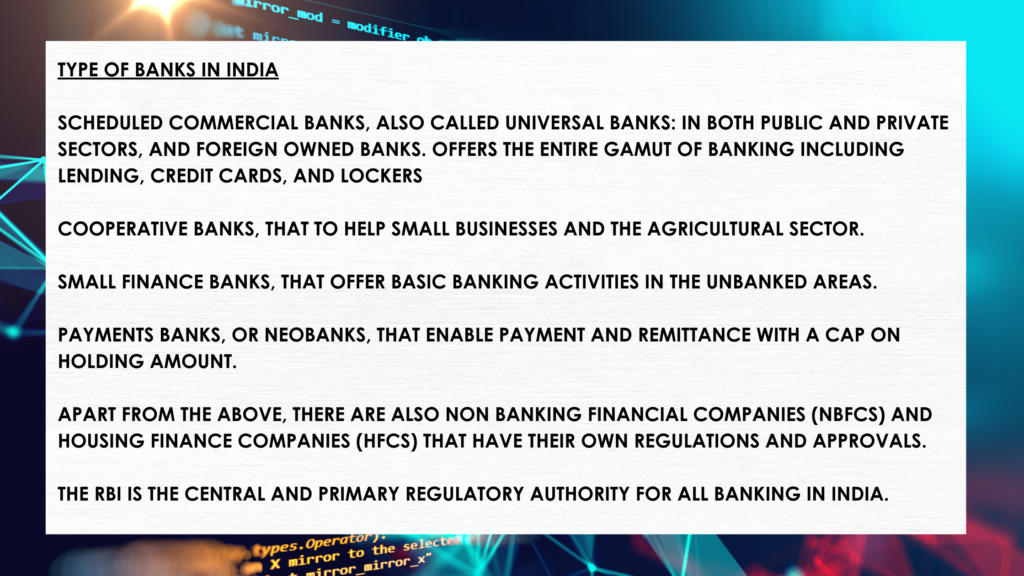

In Banking licenses, there are four categories:

(1) Commercial banks with full banking licenses that includes lending and credit cards,

(2) Small finance banks, that are offered licenses for improving financial inclusion among unbanked or underbanked people,

(3) Payments banks, which is an under-1 lakh wallet-type banks that do basic banking except lending, and finally,

(4) Cooperative banks, that are nonprofits that serve smaller businesses, and entrepreneurs, especially in the agrarian and rural sectors.

A commercial bank enjoys full banking license, in accordance with the Banking Regulations Act 1949. There are twelve public sector banks as we write this in June 2021, a number that is expected to further reduce due to mergers and privatization. Apart from the public sector commercial banks, there are also newer commercial banks that are funded by foreign investments, private sector players, and also regional rural banks (that are scheduled as commercial).

Information about banking licenses in India

Small finance banks, aimed at providing financial inclusion, are a growing lot, with ten operating entities currently, with more likely to follow.

A payments bank (also called a neobank with nearly zero physical presence, has the ability to scale quickly, and offer services through any connected device) was a model created by the RBI in 2013 and rolled out in 2015, to enable accelerated and easy transactions that could do anything except issue credit cards or loans. Customers are allowed to hold up to Rs 1 lakh (100,000), and enjoy a flurry of services to lead a cash-free life. There are more than 11 payments banks in India now, with more expected to be licensed soon.

Cooperative banks are special purpose banks that operate in both urban and rural setups. They are instituted to uplift communities, especially the small entrepreneurs and for agricultural endeavours.

Today, the banking sector is being cautiously opened up for private investors, such as senior banker entrepreneurs opening new banks, NBFCs (non-banking financial companies) or joint venture entities from the private sector being extended licenses to open banks. An important RBI publication titled ‘Guidelines for licensing of new banks in the private sector’ is a landmark step ahead in truly democratizing the banking sector in favour of extending banking services to the unbanked and the underbanked.

With the decades of solid experience and empowerment the RBI has, the public have always reposed their faith in the central bank, and have continued to support new banking ventures. With every new institutional crisis, the RBI has ensured that customers don’t suffer, and has worked to provide remedial measures, guided mergers, and consolidations in view of the larger good.

As banks have now evolved beyond brick-and-mortar buildings, and are now immensely scalable. Digital banking revolutions like the Open Banking framework and API-centric banking paradigm have enabled instant and easy document verification and extension of all banking services to every customer. Today, the banking sector continues to work towards staying relevant to the newer generation by making banking easy. More than ever before, the young banking customer expects more banking and less of bankers in their modes of interaction, typically through apps or desktop modes.

In the next decade, thanks to progressive policy making and following several success stories of new banks, including neobanks, the Indian banking sector is expected to grow out of the paradigms of the earlier century, with pathbreaking, exciting innovations seeming possible every year. With the RBI and consumer-protectionist governmental policies in place, the sector is expected to bring every citizen under the banking umbrella, which will help propel the country’s economy to greater heights.